What to know about Roseville's 2025 annual financial audit

A clean audit, with some process issues discovered

The Roseville City Council received and approved the 2025 annual financial report at the May 11 city council meeting. The report was prepared by the city's finance department and audited by an independent CPA firm. A representative from the firm presented the audit's findings to the city council.

TLDR: Roseville received a clean audit opinion, which is good. But also found process issues residents should understand.

What is a city audit? Who audits us? And what did this year’s audit actually find?

Let’s dig in:

What is a city audit?

A city audit is an independent financial checkup. It does not decide whether every city spending choice was wise, whether taxes are too high, or whether every project was worth it. It asks a narrower but important question: can residents trust the city’s financial statements?

Minnesota law requires cities to issue an annual financial report and have it audited by a licensed Certified Public Accountant (CPA) firm or the Office of the State Auditor.

Roseville currently uses Redpath and Company, an independent CPA firm.

Understanding the auditor options

For context, Roseville first selected Redpath for the 2017–2019 audit cycle after an RFP process. The 2017 staff memo said Redpath would bring “a fresh perspective” because the firm had “never audited the City of Roseville” before. It also said a three-year term was consistent with the city’s professional services policy. The city has contracted with Redpath for this audit every year since.

By using an independent CPA firm, like Redpath, the city can use a competitive RFP process, compare costs, choose a firm with municipal audit experience, and build continuity with an audit team that understands Roseville’s systems. A possible challenge of this option is achieving the desired "fresh perspective."

The City of Roseville could use the Office of the State Auditor instead. The OSA specializes exclusively in Minnesota local government law, compliance, and public sector accounting standards.

A possible challenge of this option is that depending on the size of the city and the complexity of the files, the OSA's hourly rates and overall audit fees can sometimes be higher than a competitive bid from a local private firm. Additionally, the OSA audits hundreds of entities. Because of high demand and rigid state schedules, a city may have less control over exactly when the auditors arrive or finish.

2025 Audit Reports

This year, Redpath issued four reports:

- Opinion on the Fair Presentation of the Financial Statements

- Report on Internal Controls

- Report on Minnesota Legal Compliance

- Communication to Those Charged with Governance

Plain English Translation:

- Opinion on the Financial Statements: Are the final numbers reliable?

- Internal Controls Report: Are the city’s processes strong enough to prevent or catch mistakes?

- Minnesota Legal Compliance Report: Did the city follow certain state finance rules?

- Governance Letter: What should the auditor tell the City Council directly?

In some years, there may also be a 5th federal spending report, commonly called a Single Audit.

Current federal rules require a Single Audit when a non-federal entity spends $1,000,000 or more in federal awards during the fiscal year. Entities below that threshold are exempt for that year, although records still must be available for review.

Since Roseville did not meet that threshold in 2025, that federal report was not required.

Award for Excellence

Roseville received the GFOA Award for Excellence in Financial Reporting for its 2024 Annual Comprehensive Financial Report from the Government Finance Officers Association.

“This Award demonstrates the City’s commitment to preparing financial statements that are comprehensive, transparent, and consistent with accounting standards,” according to the Redpath presentation.

What did the 2025 audit find?

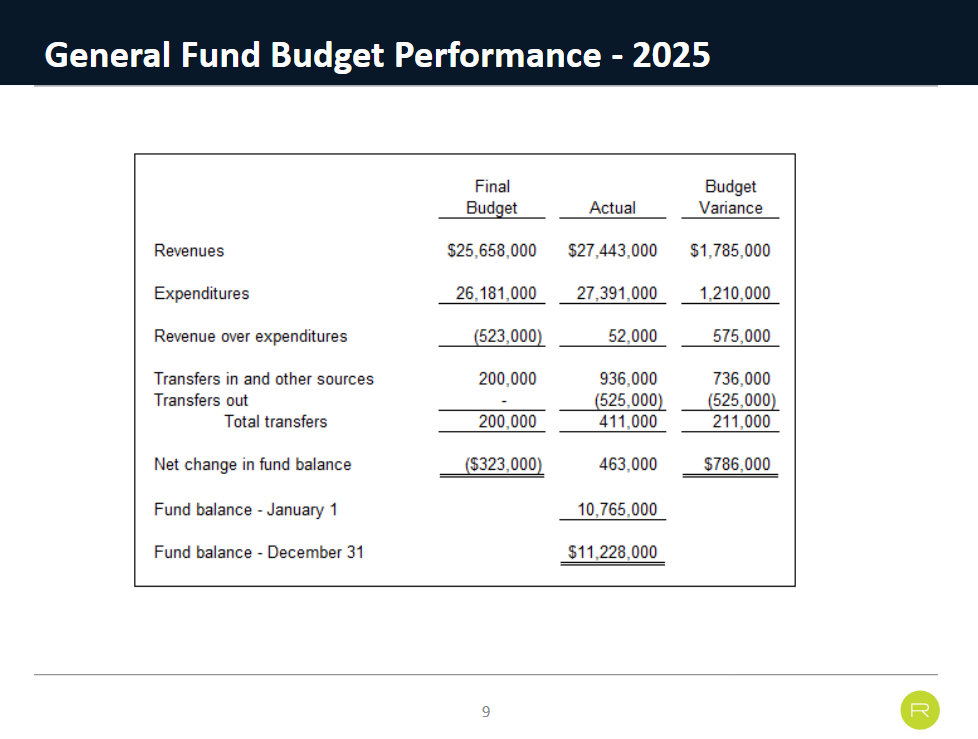

The short version: Roseville received a "clean" audit opinion, but not a perfect audit.

That distinction matters. A clean opinion means the auditor believes the final financial statements are reliable. It does not mean the auditor found nothing worth fixing.

The details: The main issue was the Water Fund. The Internal Control Report says an invoice including $977,229 of Water Fund expenses for services and charges related to a 2024 project that was not paid in 2024.

Turns out, the invoice was received by a city department, but not submitted to the finance department for payment. Those invoices should have been recorded as a liability on December 31, 2024. The invoices for the project were paid in January 2026.

Discussion

“In the world of accounting, we should have accounted for the fact that we had that liability to pay that amount for the year it was incurred and we had not done that. It’s not that we didn’t have the money, it’s that we didn’t account for the liability that the city had to pay that amount,” Mayor Dan Roe said at the May 11 city council meeting.

According to State Statute, a vendor can charge interest for an unpaid invoice. In this case, the vendor was Ramsey County, which chose not to penalize Roseville for this late payment, according to Roseville’s Finance Director Sam Magureanu.

Councilmember Robin Schroeder asked if this had any impact on the water utility rates.

Magureanu assured her that it did not, since water utility rates are determined based on long-range planning, not just the upcoming year.

“When we do our long-range planning, we’re accounting for those expenses happening 100 percent. For the purpose of determining rates, the timing of when we cut the check shouldn’t have mattered at all,” Magureanu said.

Councilmember Robin Schroeder asked if the State Auditor would need to get involved for an issue like this.

Rebecca Petersen, from the firm of Redpath and Company, LLC, said that would be unnecessary and unlikely.

“Where it really comes to light is if it was extremely pervasive. If you had ten findings, there was evidence of fraud, that’s when you’re going to hear from the state auditor. A legal compliance finding is extremely common. Something you correct and move on,” Petersen said to the city council.

The city council thanked the auditor for the report and expressed confidence that the city would learn from this mistake and improve processes and procedures moving forward.

“The fortunate thing is by catching things early, we can make the corrections and do the things we need to do to keep the finances of the city in good shape. That’s why we put those types of procedures and why we test them and adjust them as need be,” Roe said at the meeting.

There was an opportunity for public comment, but no one came forward.

More Information

For more details on the 2025 Financial Report and audit findings, view the May 11 city council meeting recording and meeting documents.

Naomi Krueger is the Roseville Reader's founding editor. She is a part time journalist with a career in publishing. She and her husband have lived in Roseville since 2014 and have two kids in Roseville Area Schools.

Prajwal “Praj” Vemireddy is a Roseville resident and chair of the City of Roseville’s Equity and Inclusion Commission. He works in finance at 3M and writes about local government to help residents better understand how their city works.

ICYMI